Profitable Farmland

Sometimes when I run out of topics to write about for the blog I would visit the fabric store to find new material. 😀 But other times, I am inspired by visitors like you! A while ago a reader requested I do a profit and loss statement for my farmland. Great idea! So today’s post is a financial update about my farm’s earnings.

As you might recall when I first bought my farmland I was losing money on it. Well, after a few years I am finally in the black! 2015 represents the first year my farmland is profitable. Yay! 🙂

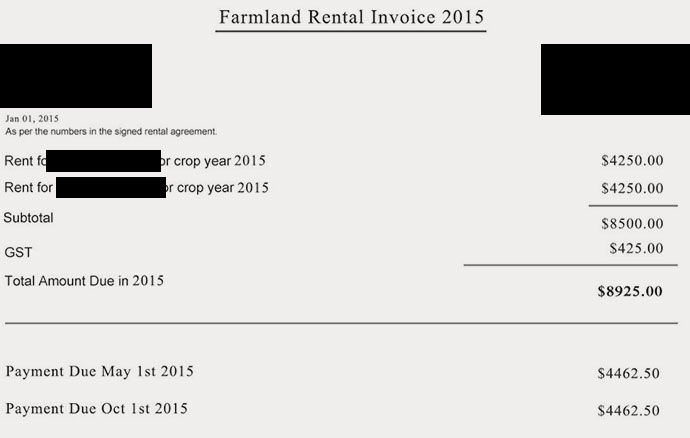

Revenue from my farmland comes in the form of rental income. Both farms are leased to the same farmer who grows crops on it every year. Expenses include interest on bank loans and property tax. There are not a lot of costs associated with owning farmland. It’s only land so there’re no buildings or lawns to maintain. Let’s take a closer look at 2015’s numbers.

Revenue is down about $1,500 from the previous year because crop prices are lower. Since the prices of soft commodities like wheat and canola have fallen I’ve agreed to lower the rent for this year. If crop prices rise in the future I will be paid more.

As for expenses, it is dramatically down this year thanks to the lower cost of borrowing. 🙂 Many were hesitant to borrow money last year because they thought when interest rates go up they will have a harder time servicing their debts.

That’s not wrong, but I don’t personally adopt that kind of mindset because timing rate hikes is a fool’s game. The central bank actually lowered rates this year, twice. So now investors like myself, who have already borrowed money, are paying less interest than before. And our investments continue to perform well. Here’s a look at my current farmland loan situation. I only have about $200,000 left to pay off.

Prior to now I was paying 3.89% interest rate on my loans. But now it is only 3.43%. 🙂 Both my loans share the same interest rate. The reason I have two loans is because I bought my farms separately – one in late 2012, and the other in 2013.

")

With my current $200,000 balance, I would only pay $6,860 a year for interest. The total property tax this year is about $1,600. However, I can save about $80 if I pay my property tax before the end of this month, which I plan to do.

So after a few years I am finally making a $100 profit! I can’t wait to spend all that money. But as I wrote back in 2012, most of the gains from farmland investing is from capital appreciation. According to Statistics Canada, from 1981 to 2014, farm asset values have increased by more than 300% to over half a trillion dollars today. Last year Saskatchewan farmland prices experienced the highest average increase at 19%. This represented about 150% return on my investment due to my 8x leverage strategy.

Finding Value in Farmland

Compared to other types of investments farmland is still an attractive long-term hold. To analyse stocks investors often use the price to earnings ratio. The lower the P/E ratio is, the more return on investment the stock should generate over time. This is a useful way to find the best-valued stocks. With farmland, we can evaluate similar metrics by using the price of land relative to its income-earning potential. So instead of using price per share, we can use price per acre of farmland. And instead of using adjusted earnings we can use cash receipts. Farm cash receipts are not the same as net income, but it does a better job at tracking the patterns in farmland values. Below is a chart showing the average P/E ratio in different provinces over time.

It appears farmland values in Ontario and Quebec are off the husk! They are like the Netflix and Tesla Motors of farmland in terms of valuation, lol. If someone wanted to buy farmland in Canada today I would recommend maybe looking in Saskatchewan first. It’s hard to say how much farmland prices will continue to climb. But studies indicate that although growth should slow down going forward, moderate price increases are still to be expected in certain parts of the country.

Sources: Personal experience and the Farm Credit Canada summer 2015 report (Download PDF file)

———————————————————–

Random Useless Fact:

A University of Guelph study found that more than 50% of undergraduate students, and 35% of graduate students admit to cheating on written work.

{kind=link}

Nice write up your farmland investing. Glad to see you in the black now. I also like that the loans are with TD Bank, since I am a shareholder :).

I’m a shareholder as well. Although currently I give them a lot more money in interest than they give me in dividends lol. But one day the tables will turn.

Awesome article. When you were looking for farmland how did you find it? Most of what I see on MLS comes with a farm, where did you look to find just the land? How did you figure out if it was good value? Also how did you find a farmer to rent from you? Was it more difficult than renting out a property? My husband and I currently rent out a town home and were originally planning to buy a second one, but now we’re thinking that farmland may be a better way to diversify.

I found it on MLS under the agricultural section. Some farmland comes with buildings, others are bare land. If you filter “cash crop” you should be able to find some good quality land. Or, call one of the real estate agencies around the location you’re looking for and have one of their brokers do the leg work for you. 🙂 I figured it was good value because I compared the assessed value of the farm with other farms around the same area. All land is split into roughly the same sized squares in Saskatchewan so when size is a constant, any differences in the assessed price is due to the varying quality of each parcel of land. This website has the government assessed value of all farmland in the province. sama.sk.ca/sama/Map.aspx. After I made certain the value was relatively competitive with neighboring farmland I looked at other listings around the area and determined that the asking price the seller wanted was reasonable and not out of line with market trends. Luckily for me, there was already a farmer on the land. I just renewed the lease agreement that he had with the previous owner and he kept on farming it.… Read more »

How does it look like from a cashflow point of view ?

From what I understood, you revenu basicly match you interest cost plus tax expenses. So basicly aside from appreciation, all the equity you are building is comming out of your pocket.

Seems like more risk than I would be confortable with to have only appreciation to look for.

If you think farmland is risky then you don’t understand farmland, which is much less risky than public equity.

I was not comparing it to stocks, just analysing it as a real estate investment.

When your normal operation is running at break even profit (revenu = expenses + interest), you can only count on potential appreciation.

I think it’s risky because basicly if anything goes wrong (renter stop paying, interest rise,…) you end up losing money big time. And if you don’t have appreciation, you took all those risks for no gain.

I can understand negative cashflow, but zero profit aside from appreciation is pushing the limit of leverage a little too far imho.

But as anything with levage, the gamble can also be very lucrative if the market moves the way you want it.

My cash flow is negative $500 per month haha. All of that money is going to equity building.

I went to Ladner for a Segaway tour. Lots of farmlands there, I see some pretty impressive houses going up there. Farmers must be doing something right there 🙂 I personally wouldn’t invest in a farmland as I don’t want to be so much indebted. But good on you for making it work for the longer term investing.

Yeah, BC farmers are some of the richest Canadians ever, especially if they’ve owned land for a long time. Thanks for telling me about your Segway experience. I’ll probably look more into it when I go plan to visit Ladner next time. 🙂

I have been following your blog for a while after I noticed you had bought some farmland. Not too many personal finance bloggers out there in the agricultural market. A couple things I noticed on this recent post: first is do you have a 6 month variable interest rate on your farm loans? Probably has been good so far, but do you have the option to lock the rate if you choose? Here in the US, crop prices have been on the decline for the last year or two, and it looks like things might continue to be down for another couple. Could you do a multi-year lease to lock in your rent?

Yes, I have a 6 month variable rate since that is the lowest I could get. 🙂 I do have the option to lock it in for 2 or 3 years and get a fixed interest rate which will probably be 1% to 2% higher than my current rate. Crop prices in Canada has gone down over the last few years as well. I would like to do a multi-year lease but my tenant will only sign one year contracts. Right now I don’t have any other interested party to rent my farm.

Nice post. Can you add some color on the financing aspects of farmland? Were there any challenges you experienced getting it financing? How much was TD willing to lend (LTV)? How does farmland get appraised for lending purposes (cash flow, something else?). Are there certain characteristics of the property that the bank looks at (grades maybe?). Is there any difference if you rent it out vs. operate the farm yourself? Thanks

I read with much interest your investment in farmland. In order to diversify I would like to invest in a farmland REIT rather than myself buying land but there doesn’t seem to be any available in Canada (in US there are quite a few farmland REITs).

I’ve found a few private investments but they are closed now.